Implied Volatility (IV) and Historical Volatility (HV)

Volatility, or how fast prices change, is often seen as a way to gauge market sentiment, and in particular the degree of fear among market participants.

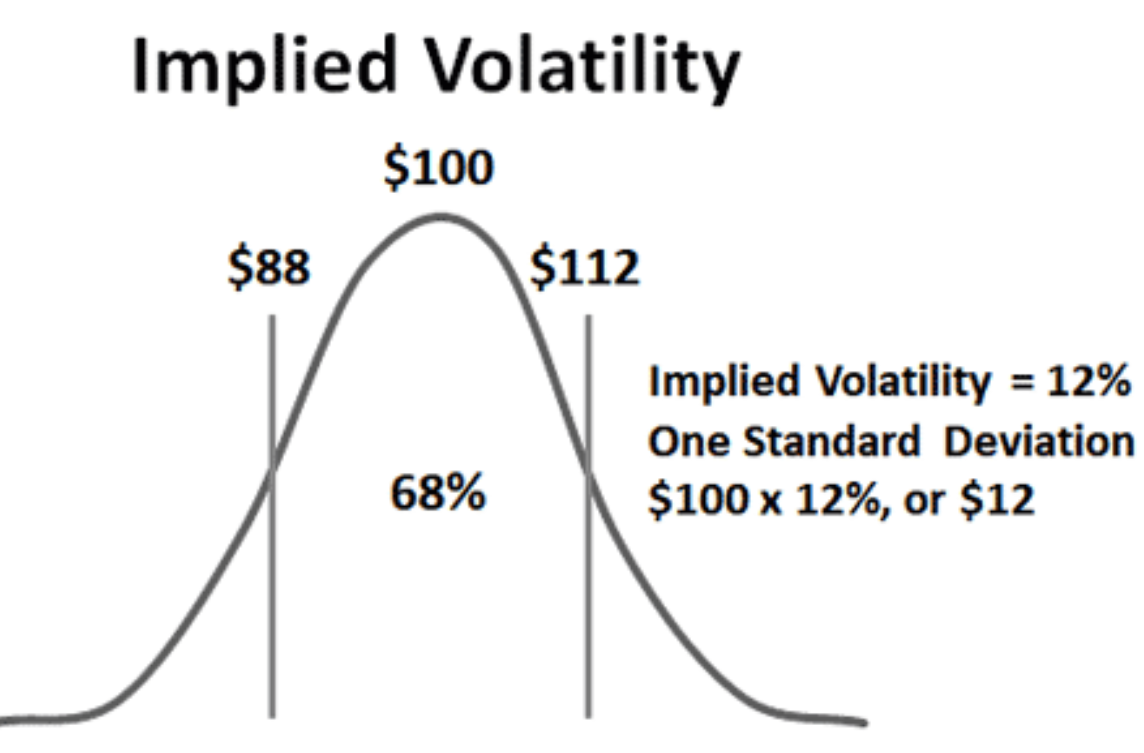

The Implied volatility (IV) is based on the option prices of stocks. These options include projected prices and expiration dates, so they can be used to measure expected sentiment and likely volatility of a stock.

The Historical Volatility also measures variations in prices but based on actual historical data.

So, IV is a forward-looking measure implied by the options market, and HV is backward looking.

An IV that’s lower than HV could suggest that IV is understating the stock’s potential price change. An IV that’s higher than HV could suggest the opposite.

Further, a low IV percentile could indicate that options premiums are relatively low, and there might be opportunities to go long.

IV can also be used to define the bounds of profit takes. One should not aim to gain more than what the volatility is likely to achieve.

Figure 6.11: Implied volatility